Perhaps talk of a full economic recovery is premature as global unemployment issues will continue well into 2010, however many investors are again viewing their chances of growth in emerging markets as better than those of the United States or Europe. In particular, India, China and Brazil stock markets have shown leading gains since March 2009.

As a result, the Indian Nifty stock index has jumped by 64% in the last three months. China CSI 300 index of shares in Shanghai and Shenzhen have risen 37% and Brazil’s Bovespa increased 41%

over the same period. By comparison, the Standard & Poor’s 500’s gained about 28% returns.

Although these emerging markets may face some issues, by and large they are manageable issues. For example, the Prime Minister of India, Manmohan Singh said Wednesday while in the Lok Sabha that India will achieve economic growth of at least 7% this fiscal year.

On Wednesday, the S&P CNX India Nifty rose 121 points or 2.73% to 4,551 on the Bombay Stock Exchange - Twenty eight out of 30 India’s Sensex stocks ended in the green including DLF(up 10.07%), Jaiprakash(up 8.18%), Reliance Communication(up 7.37%), Larsen & Toubro(up 6.39%), Ranbaxy (RBXLF.PK) up 6.37%, Mahindra & Mahindra(up 6.34%), TCS(up 5.95%), Tata Power(up 5.55%), Tata Steel (TATLY.PK) up 5.28%, Hindalco(up 4.53%) and ACC(up 4.47%) were the top gainers. Grasim Industries (GRSXY.PK) and NTPC ended down around 0.60% each.

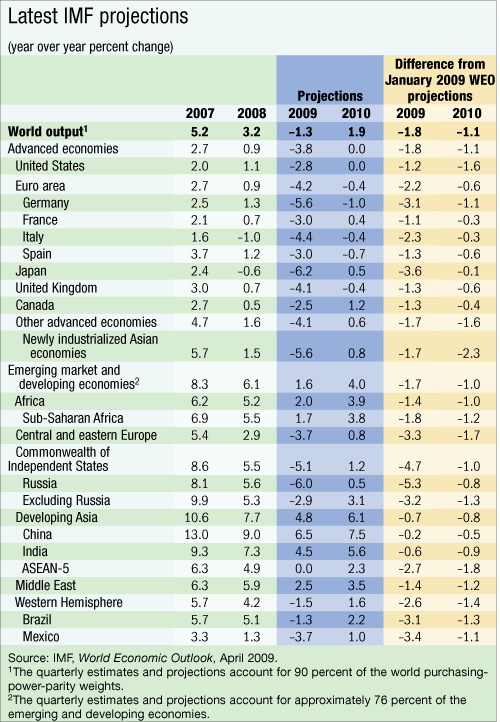

Additional support for this emerging market growth is found in the recent IMF (World Economic Outlook Report, April 2009) that calculates global growth is projected to reemerge in 2010, but at 1.9 % rather sluggish relative to past recoveries. The IMF states that global growth in 2010 would come entirely from the emerging markets and developing countries such as India, China and Brazil, at an average of 4%, while developed countries' such as the U.S. and Europe economies are expected to remain stagnant or less until at least 2010.

Click to enlarge:

Today, the MSCI Brazil Index (EWZ) closed at $55.63. Brazil Bovespa Stock Index is up 54%. EWZ June option implied volatility is at 58 July is at 53; below its 26-week average of 61.

Across the world, banks are limiting access to credit (and will continue to do so) as the overhang of bad assets and uncertainty about which institutions will remain solvent keep private capital on the sidelines. Funding strains have spread well beyond short-term bank funding markets in advanced economies. Many nonfinancial corporations are unable to obtain working capital, and some are having difficulty raising longer-term debt.

The broad retrenchment of foreign investors and banks from emerging economies and the resulting buildup in funding pressures are particularly worrisome. New securities issues have come to a virtual stop, bank-related flows have been curtailed, bond spreads have soared, equity prices have dropped, and exchange markets have come under heavy pressure.

Beyond a general rise in risk aversion, this reflects a range of adverse factors, including the damage done to advanced economy banks and hedge funds, the desire to move funds under the ‘umbrella’ provided by the increasing provision of guarantees in mature markets, and rising concerns about the economic prospects and vulnerabilities of emerging economies.

On the upside, however, bold policy implementation that is able to convince markets that financial strains are being dealt with decisively could revive confidence and spending commitments. But even when the crisis is past, there will be a difficult transition period, with output growth appreciably below rates seen in the recent past.

The greatest policy priority at this juncture is financial sector restructuring. Convincing progress on this front is crucial for an economic recovery to take hold and would significantly enhance the effectiveness of monetary and fiscal stimulus.

The critical underpinning of an enduring solution must be credible loss recognition on impaired assets. To that effect, governments need to establish common basic methodologies for the realistic valuation of securitized credit instruments, which should be based on expected economic conditions and an attempt to estimate the value of future income streams.

Recapitalization methods must be rooted in a careful evaluation of the long-term viability of institutions, taking into account both losses to date and a realistic assessment of the prospects of further write downs.

No comments:

Post a Comment