Its defensive nature helped the FMCG sector perform well even in these tough economic times. Here are some basic facts about some of our stock picks in this sector

- Marico Sales for the company crossed Rs 2,000 crore this financial year

- Britannia Inds Higher wheat and sugar prices may pose problems

- Colgate-Palmolive Focus on core business will give company a steady income stream

- Gillette India Strong brand value, but at 26 times earnings it’s a little expensive

- P&G Hygiene & healthcare Recorded 20% growth in net sales

- QSK Consumer Healthcare Improved its operating margin to 25.54% against 18.01% in the previous quarter

- Emami It can draw synergies from Zandu, which it acquired last year

- Hindustan Unilever Net sales during the quarter managed to grow only at 6%

- Dabur India Profit growth was at 31% as operating profits increased

***

The equity markets have bounced back sharply from their lows, but are still down 42 per cent from the peak of January 2008 and 28 per cent from the levels a year back. Typically, in a downturn, the focus shifts from the price of a stock to its earnings. In times when the financial sector and the real economy are in trouble, and the risk appetite is low, investors are willing to pay a premium for predictability of earnings. The last year was a witness to this trend.

Due to their defensive nature, the fast-moving consumer goods (FMCG) and the pharmaceuticals sectors stood out on performance during this difficult period. Anticipating this sectoral shift, we started recommending stocks from these sectors from late 2007. In this issue, we revisit our picks from the FMCG space in the light of the fourth quarter results for financial year 2008-09 (Q4FY09) and give fresh recommendations at their current levels.

***

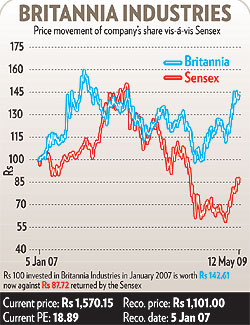

Britannia Industries

The collapse of Lehman Brothers in mid-September last year intensified the global financial crisis and stockmarkets across the world slipped sharply to lows from which they are still struggling to recover. Even in this scenario, some defensive stocks, such as Britannia Industries bucked the trend. From around Rs 1,080 in October, the stock has moved up to its current level of around Rs 1,550.

The collapse of Lehman Brothers in mid-September last year intensified the global financial crisis and stockmarkets across the world slipped sharply to lows from which they are still struggling to recover. Even in this scenario, some defensive stocks, such as Britannia Industries bucked the trend. From around Rs 1,080 in October, the stock has moved up to its current level of around Rs 1,550.

We recommended this stock in January 2007 at Rs 1,101. It went up all the way to Rs 1,700 in December 2007, but corrected to Rs 1,316 by September 2008 due to fears of hyperinflation. Though the fear of inflation has eased, higher wheat and sugar prices may continue to pose problems. The company’s March quarter numbers are expected to be out on 30 June 2009; the December quarter numbers did show pressure on margins. The operating margins contracted about 100 basis points.

We recommend a hold on this counter as the company is witnessing good volume growth. Volumes were up 12 per cent in the December quarter, while total sales were up 25 per cent. Also, decline in crude prices will help save on packaging cost.

Our recommendation: Hold

***

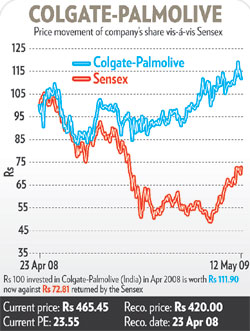

Colgate-Palmolive (India)

Colgate has focused solely on its core strength—oral dental care products. Through its marketing efforts, the company has retained the top position in product categories such as toothpastes and toothbrushes.

Colgate has focused solely on its core strength—oral dental care products. Through its marketing efforts, the company has retained the top position in product categories such as toothpastes and toothbrushes.

It also undertakes marketing initiatives at regular intervals to increase consumption of oral care products, which has helped it sustain growth in both rural and urban areas. In the first three quarters of FY09, the company’s sales grew sequentially. On yearly basis, sales growth averaged 15 per cent and the average profit growth was 20 per cent.

One of the company’s strengths is its ability to cut costs at all levels. Even in 2007-08, when rising commodity prices were putting downward pressure on the margins of most FMCG companies, Colgate kept its operating margin intact by improving company-wide efficiency and cutting costs. Given its consistent business performance and returns to shareholders, we re-recommended Colgate-Palmolive (India) in April 2009. We first recommended it in April 2008.

Currently, the company’s scrip is priced at 24 times its trailing 12 months’ (TTM) earnings, which is a bit higher than the April 2008 level. Along with the price rise, the company should be able to maintain high growth in its earnings. From that perspective, the stock does not look expensive even at its current PE. However, at this level, you could also book some profits and re-enter later at a lower price.

Our recommendation: Book Your Profits

***

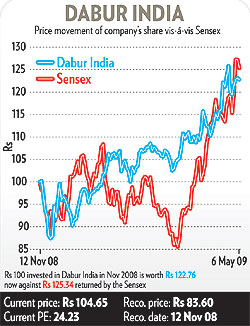

Dabur India

We recommended Dabur India in November 2008 at 20.91 times its TTM earnings. Although the valuation seemed high as compared to the then depressed market, expectations of steady returns made it a case for investing. The scrip has moved up around 25 per cent since then and is now commanding a PE of 24.

We recommended Dabur India in November 2008 at 20.91 times its TTM earnings. Although the valuation seemed high as compared to the then depressed market, expectations of steady returns made it a case for investing. The scrip has moved up around 25 per cent since then and is now commanding a PE of 24.

During Q4FY09, the company’s consumer care business, which accounts for the bulk of its revenue, grew at a robust 20 per cent. As a result, the overall revenue, too, went up 20 per cent. The profit growth was higher at 31 per cent as the profitability of operations increased.

Dabur is known for herbal products in the personal care and healthcare categories. Although herbal products account for around 85 per cent of its revenue, the company is also focused on developing non-herbal products such as fairness creams.

The company has not restricted itself to organic growth and continuously looks for acquisitions to mark its presence in new markets and new categories. Its international division has reported a strong growth of around 40 per cent. It had a presence in North Africa and has now entered high-potential markets such as China, Turkey and Lebanon.

The Indian market continues to have huge potential in the form of the under-penetrated rural market. Growth in the rural segment, which forms 32 per cent of the FMCG market, would support the company’s current growth momentum. Considering this, the stock should have a place in your portfolio.

Our recommendation: Hold

***

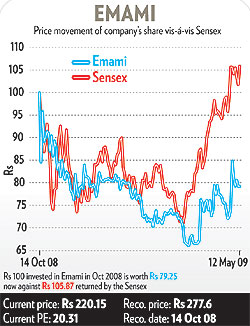

Emami

A major player in personal and healthcare business, Emami focuses on ayurvedic products backed by modern manufacturing technology. We recommended its scrip in October 2008 at 18 times its TTM earnings when it was in process of acquiring Zandu Pharmaceutical Works.

A major player in personal and healthcare business, Emami focuses on ayurvedic products backed by modern manufacturing technology. We recommended its scrip in October 2008 at 18 times its TTM earnings when it was in process of acquiring Zandu Pharmaceutical Works.

The acquisition is now complete—Emami paid around Rs 750 crore to buy a 72 per cent stake in Zandu. The amount seems large compared with Emami’s

Rs 650-crore annual revenue in FY09. However, the acquisition will add value to the company in the long run.

It would add to both the topline and bottomline of the company. This is already reflected in the company’s consolidated earnings figures (including Zandu) for FY09. The consolidated net sales increased by 28 per cent year-on-year (y-o-y). Emami’s operating profit was up 37 per cent due to improved business profitability.

Emami’s standalone (excluding Zandu) sales and operating profit also showed a healthy growth of 11 per cent each. In FY09, the company accounted for interest outflow compared with interest inflow in the previous year. The net effect was high interest expenses growth in FY09, which eroded its profits.

Emami continues to maintain the lead position in most of its product categories. Zandu would further add to its portfolio of ayurvedic products. Considering the stability of Emami’s business, at the current PE of 20, its stock is still attractive.

Our recommendation: Hold

***

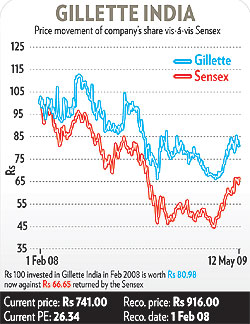

Gillette India

Gillette’s business seems shielded from the effects of the downturn. The Q4FY09 results are a proof. Its male grooming products, including razor blades, reported a revenue growth of around 14 per cent y-o-y. The oral care segment grew robustly at 59 per cent. The relatively smaller segment, portable power, grew at a healthy 19 per cent. Overall, the company’s net sales and profit grew at 22 per cent and 27 per cent, respectively.

Gillette’s business seems shielded from the effects of the downturn. The Q4FY09 results are a proof. Its male grooming products, including razor blades, reported a revenue growth of around 14 per cent y-o-y. The oral care segment grew robustly at 59 per cent. The relatively smaller segment, portable power, grew at a healthy 19 per cent. Overall, the company’s net sales and profit grew at 22 per cent and 27 per cent, respectively.

We had recommended Gillette at a PE of 22.79 in February 2008. Since then, the stock has lost 19 per cent of its value. On the other hand, the PE has moved up to 26.34. This means that the EPS has come down. At its current PE, the stock looks expensive.

Our recommendation: Sell

***

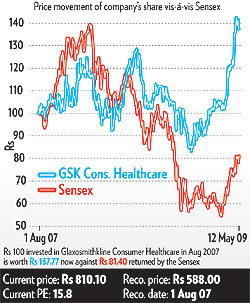

Glaxosmithkline Consumer Healthcare (GSK)

We recommended this stock in August 2007 at Rs 588, and maintained a buy on it in our issue dated 9 April 2009. The stock continues to attract buying interest.

We recommended this stock in August 2007 at Rs 588, and maintained a buy on it in our issue dated 9 April 2009. The stock continues to attract buying interest.

Backed by robust numbers for the March 2009 quarter, the stock has moved from Rs 716 in mid-April 2009 to the current levels of Rs 810. In the March quarter, the company registered a sales growth of 31.28 per cent, while net profits were up 48.35 per cent, which was above expectations.

The company also improved its operating margin in the March quarter to 25.54 per cent against 18.01 per cent in the previous quarter. Its net margins reached 14.85 per cent from 9.11 per cent during the same period.

During the March quarter, the company added two products to its portfolio—Horlicks Nutribar, a nutritional snack for health conscious people, and Actigrow, a high-protein baby food. Also, Boost is the official energy drink of Rajasthan Royals in the Indian Premier League (IPL).

We maintain a buy recommendation on the stock. Though prices may go down in the short term as they went up very quickly last month, the stock is expected to touch new highs in the long term due to volume growth and better margins. Also, at the end of 2008, the company had cash in excess of Rs 470 crore, which can be used for expansion or for disbursing higher dividends.

Our recommendation: Buy

***

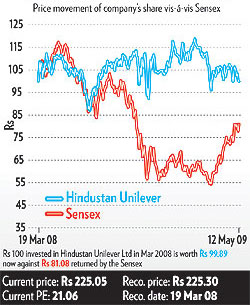

Hindustan Unilever (HUL)

We recommended HUL in March 2008. The stock has not appreciated much on a year-to-date basis since then, but it has protected shareholders’ capital. It went on to touch Rs 268 in February 2009 from Rs 225 in April 2008 when we had recommended it. The stock corrected after February 2009 and is currently trading at Rs 225.05.

We recommended HUL in March 2008. The stock has not appreciated much on a year-to-date basis since then, but it has protected shareholders’ capital. It went on to touch Rs 268 in February 2009 from Rs 225 in April 2008 when we had recommended it. The stock corrected after February 2009 and is currently trading at Rs 225.05.

The company is out with its fourth quarter results for FY09 and the numbers are below street expectations. Net sales during the quarter only managed to grow at 6 per cent, largely due to a 45 per cent decline in the value of exports. The management says that the decline in non-core exports is part of a strategy. Profits after tax before exceptional items went up 20 per cent.

However, profits after exceptional items were flat. Operating margins did improve by 200 basis points, largely due to lower input prices. So, the current price of Rs 225.05 is about 21 times its earnings. Maintaining the growth looks difficult in view of disappointing sales numbers. We would recommend you reduce exposures.

Our recommendation: Reduce Holdings

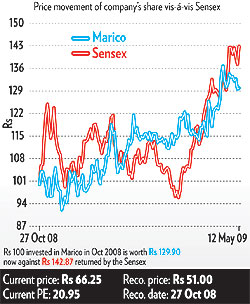

Marico

Riding its strong portfolio of brands such as Parachute, Nihar and Saffola, Marico has posted a topline growth of 25 per cent to cross the Rs 2,000-crore mark in this financial year for the first time; its volume growth was 12 per cent.

Riding its strong portfolio of brands such as Parachute, Nihar and Saffola, Marico has posted a topline growth of 25 per cent to cross the Rs 2,000-crore mark in this financial year for the first time; its volume growth was 12 per cent.

Parachute and Nihar, the leading brands of the company, grew 9 per cent during the financial year and maintained their market share of 48 per cent in the Rs 1,500-crore branded coconut hair oil market. Among other businesses, Kaya Skin Clinic, which has 74 branches in India and 11 in the Middle East, registered a turnover growth of 57 per cent in FY09. Though it ended the year with a loss of Rs 1.6 crore (due to opening of new clinics), the company expects Kaya to contribute to the bottomline in FY10.

We recommended Marico at a price of Rs 50.65 on 27 October 2008. The stock is currently trading at Rs 66.25. We maintain a hold on this counter as the company is expected to maintain its growth momentum.

The company took a Rs 15-crore hit in profits due to the divestment of Sundari, its spa products business, which Marico acquired in 2003. But, going forward, The company expects to improve operating margins with raw material prices easing significantly. Marico declared a dividend of 65.5 per cent during FY09.

At the end of FY09, Marico had a gross debt of Rs 375 crore, of which Rs 200 crore is dollar denominated. The management is confident that it has adequate cash flow to maintain healthy debt service coverage.

Our recommendation: Hold

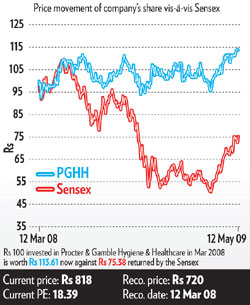

Procter & Gamble Hygiene & Healthcare (PGHH)

We recommended the stock in March 2008 at a PE of 20. A year later, the stock has barely moved up by 3 per cent. However, considering the defensive nature of FMCG stocks and the unclear direction of the market, we reiterated our buy call on the stock.

We recommended the stock in March 2008 at a PE of 20. A year later, the stock has barely moved up by 3 per cent. However, considering the defensive nature of FMCG stocks and the unclear direction of the market, we reiterated our buy call on the stock.

PGHH’s two-brand portfolio has Vicks and Whisper. These are leaders in their respective categories and have huge untapped market potential. Whisper, a female hygiene product, controls around 50 per market share in urban areas. To further build a large customer base, it is reaching out to schoolgirls. Also, it is increasing the product awareness by offering samples in government schools. These steps would help the company grow its volume in the high-potential female hygiene market—just two out of 10 women in urban areas use branded pads.

PGHH’s other over-the-counter health product, Vicks, has also led the category since its inception.

In Q4FY09, the company’s net sales grew 20 per cent. The costs were under control and operating margins were stable compared to the previous quarter. Net profit growth was particularly robust at 27 per cent.

It is unlikely that PGHH’s business momentum will get hit in a major way because of the economic slowdown. Considering this kind of stability and a relatively low PE of 18, the stock remains a good investment.

No comments:

Post a Comment