The last two quarters were a rough phase for Indian companies, particularly the mid-sized ones. They witnessed a fall in demand and, at the same time, were hit hard by the high cost of funds. As a result, long-term investments got delayed and most companies found it difficult to run even day-to-day operations.

However, KS Oils, a mid-sized edible oil producer, emerged safe and sound from this phase. Neither did its sales dip, nor did it register a huge debt on its books, which could have severely affected the company due to the high cost of funds.

Business performance. KS Oils produces and sells mustard oil, soyabean oil and palm oil under brand names such as KS Gold, Kalash and Double Sher. These brands have a strong hold in the eastern and north-eastern parts of the country. Now, the company is trying to establish itself in central and northern India, too.

The edible oil market is a long-term opportunity for the company. The industry’s size is estimated at Rs 67,500 crore and is growing at 6 per cent per annum. Of this, branded oil constitutes just 15 per cent, leaving plenty of room for growth for a player like KS Oils. Also, the branded segment of the market is expected to grow at around 20 per cent with more and more people becoming health conscious. KS Oils has already gained traction in the total mustard oil market by holding a 7 per cent share even when 75 per cent of the market is unorganised. In the branded mustard oil segment, KS Oils holds 25 per cent market share. Its competitor brands in this category are Dhara and Dalda.

KS Oils is an integrated oil producer: it sources oilseeds, owns a manufacturing and refining unit and has a strong distribution network to push its products. It has recently acquired palm plantations in Malaysia and Indonesia. This would secure the supply of raw material and, to some extent, shield the company from volatility in commodity prices. It is planning to raise money to develop new manufacturing facilities that would support its expansion in cottonseed and sunflower oil.

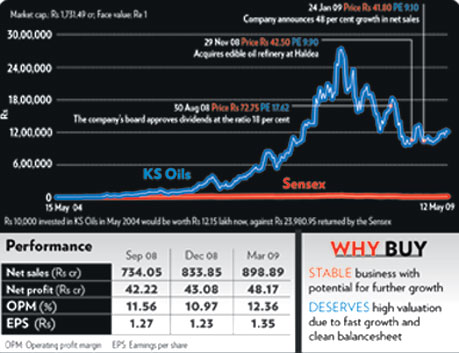

Financial performance. KS Oils has grown rapidly in the past few years. The compounded annual growth of its total income from financial year (FY) 1999 to FY08 is 22.38 per cent. Its net profit rose even faster at 65 per cent, while the operating margin expanded from 2.74 per cent in FY99 to 11.26 per cent in FY08.

Its performance in the last four quarters demonstrates its ability to do well even in bad times. Its net sales registered 7.44 per cent sequential growth during this period. Profit growth was moderate at 4.7 per cent. On a year-on-year basis, net sales and net profit grew 60 per cent and 47 per cent, respectively.

The debt-equity ratio came down from 3.77 in FY03 to 0.52 in FY08, which is a good signal. Additionally, the cash flow from operations increased from Rs 10.51 crore to Rs 57.23 crore during the same period. The total cash balance at the end of FY08 was Rs 150 crore. Low debt and adequate cash level helped it function smoothly during the bad phase.

Valuation rationale. The company’s share price has seen a sharp correction from the high of Rs 125 in January 2008. Currently, the stock is trading at 10 times trailing 12 months’ earnings at Rs 49. At this level, the scrip is discounted far more than those of other fast-moving consumer goods (FMCG) companies operating in the edible oil market. Also, considering that the company is growing fast and is less leveraged, it deserves a higher valuation.

Given its stable business model and the long-term opportunity in the edible oils business, KS Oils is a long-term buy.

No comments:

Post a Comment