Why Buy

- Axis Bank High business growth, low cost of funds, expanding NIM, improving asset quality

- Bank of Baroda High growth in advances, best asset quality among PSU banks, high NPA provisioning, less volatile treasury income

- HDFC Bank Consistently high growth, lower net NPA percentage compared to its peers, higher provisioning of NPA, large CASA base, high NIM

- Punjab National Bank Low cost of funds, high yield on loans, maintains NIM in all conditions, higher NPA provisioning, less volatile bond portfolio

- Yes Bank Lowest NPA percentage among listed banks, high growth, healthy NIM in spite of low CASA base

***

The Indian banking industry, unlike its peers in the West, came out relatively unhurt from the global financial crisis. The stocks, however, did correct a bit on the concerns of rising non-performing assets (NPAs) and loan restructuring. But, with the fear subsiding and the economy getting back to the higher growth path, there is renewed interest in the sector. The reasoning behind this is, if India has to grow at over 8-9 per cent, companies will need funds for expansion. In the absence of a vibrant bond market, they will have to tap banking sources for funding their needs. Therefore, investors are looking at this sector as a proxy to the India growth story. So, if you are also eyeing gains from the India growth story through the banking sector, we tell you how to look at stocks in the banking sector, and profile five banks we like at this stage.

Parameters

Core business. The core business of a bank is to lend, so it’s important to see how the advances have grown in the past, at least in the last few quarters. Looking at the growth in the interest income will also give you a fair idea. But, remember, this only a necessary but not a sufficient condition. Says Rajiv Mehta, research analyst at IndiaInfoline: “If a bank is growing at, say, 5-10 per cent faster than the industry, we try to analyse how it manages its margins and asset quality.” There is a possibility that to gain market share the bank might be ignoring the quality of lending.

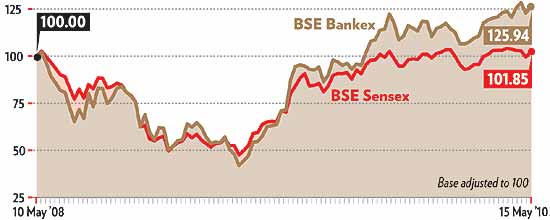

Crests And Troughs

Although banking stocks fell along with the overall market as global crisis intensified, it has rebounded sharply and outpaced the overall market on prospects of economic recovery.

Asset quality. In banking, asset quality is of prime importance and looking only at profitability is not enough. “It [profits] is not the right criterion to look for a good bank; you should rather look at the balance sheet,” says Arun Khurana, manager, banking sector fund at UTI MF. He uses the example of Vijaya Bank. For FY10, it reported a profit of Rs 502 crore, or Rs 240 crore higher than the previous year’s profit of Rs 262 crore. Thus, its profit almost grew by 92 per cent. But, at the same time, its net NPA also grew by Rs 289 crore. Khurana suggests that one should reduce net profit by increase in net NPA to get the real profit figure because the bank is not sure whether it will recover NPAs. Also, from September 2010, banks will have to provide for 70 per cent of gross NPA, which will dent profits significantly for banks not making sufficient provisioning at this stage.

Net interest margin (NIM). It is a measure of the bank’s profitability, and is calculated as net interest income (interest income minus interest expenses) divided by interest yielding assets. This checks the bank’s ability to price loans at higher rates, which is also function of bank’s ability to mobilise low cost deposits—current account and saving account (CASA). The higher the CASA ratio, the better it is. Also, as we are moving into higher rate scenario, CASA will become even more important. Says Vaibhav Agrawal, vice-president, research, at Angel Broking: “As interest rates go up, the banks with the highest CASA account will perform the best.”

Other income. There are two big components of other income: fee income and treasury income. Although growth in fee income can be predicted somewhat, treasury income is relatively volatile. It depends on the wider interest rates situation in the economy, and is also affected by various factors like the monetary policy and government borrowing. As banks in India are required to keep 25 per cent of their demand and time liability in government securities, the overall effects of bond price movement can only be managed a little.

The road ahead

Unanimous projections. The fiscal year 2010 wasn’t too good for the banking industry in terms of loan disbursal. It remained subdued for most of this period, even as growth in credit fell to single digits at the end of October 2009. But later, as economic activity picked up, credit growth accelerated to around 17 per cent at the end of the financial year. Analysts expect it to remain robust. The offtake is once again expected to come from the infrastructure space, which, after a lull, has started witnessing higher activity. “Banks have raised capital in the previous year. Further, the government’s decision to infuse capital into some banks would increase their limit for infrastructure lending,” says Rajrishi Singhal, head of research and policy, Dhanlaxmi Bank.

Treasury Tricks. When the RBI followed the policy of lower interest rates to bring growth on track, the yield on government bonds came down. As a result, banks made huge profits on bond portfolios. However, that trend has reversed now. The yields have risen significantly, with impacts already visible on banks’ result for the March 2009 quarter. Most banks have suffered losses on bond portfolios. Analysts believe that in the coming quarters, too, the bond yield will remain high and it would be difficult for banks to show treasury gains. But yields are not expected to harden too much from here on. Economists expect yields on 10-year government paper to move at most to 8.5 per cent from the current 7.8 per cent. So, major negative surprises can be ruled out. Also if the government raises the FII limit in G-secs, as reported by the financial media, greater demand will raise their prices, thereby restricting the rise in yield.

Maintaining Margins. The net interest margin rose in FY10. One of the causes behind this rise was the high proportion of low-cost CASA deposits in the overall deposit base. As rates on term deposits were low, it became less attractive, and the share of CASA increased.

However, as term deposit rates have started to rise again, banks will face difficulty in maintaining the CASA level, even as pressure might be compounded by the lag that exists in adjustment of lending and deposits rates. Suresh Ganapathy and Mudit Painuly of Macquarie Equities Research, say in a recent report: “The previous interest rate cycle was testimony to the hypothesis that lending rates, particularly in the case of Indian banks, react with a two or three quarter lag, compared to deposit rates. We expect this lag, coupled with an increase in savings rates, to exert pressure on margins in FY11.”

Banking Picks

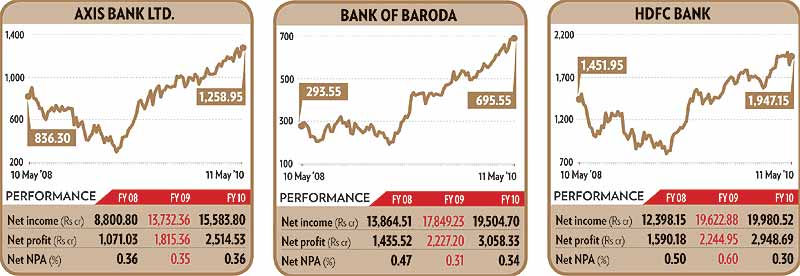

Axis Bank. It posted another quarter and year of impressive numbers. March 2010 was the 22nd quarter in a row when the bank posted net profit growth in excess of 30 per cent. During the year, net profit went up by 39 per cent, while the net interest income was up 36 per cent, showing growth of 47 per cent in 5-year CAGR. Similarly, the fee income for the bank grew by 51 per cent CAGR over the five years ending FY 10. The bank continues to maintain good asset quality with net NPA at 0.36 per cent compared to 0.75 at the end of FY06. During the fourth quarter, advances for the bank grew by a healthy 28 per cent over the previous year, against the industry’s growth of just about 18 per cent. The cost of funds also declined to 4.54 per cent against 6.64 per cent in Q4FY11, which led to improved net interest margins of 4.09 per cent.

On 12-month trailing earnings, the stock is trading at 18.78 times. Given that is consistently growing at over 30 per cent, the stock does not look too expensive.

Bank of Baroda. Bank of Baroda, or BoB, is a preferred pick in the public sector. A higher concentration in industrialised states such as Maharashtra and Gujarat gives greater push to its business. In FY10, deposits grew 25.3 per cent over the previous year. The yearly growth in advances was lower than the previous year, but, at 22.2 per cent, it was still higher than the average for the banking industry. The asset quality remained high, with net NPA at 0.34 per cent of the net advances, which is the best among PSU banks. The bank maintains a strong balance sheet by provisioning 74.90 per cent of NPAs. Another positive aspect of this bank is the low volatility of its treasury income, unlike other PSU banks, as it categorises most securities as held-to-maturity, which are not marked-to-market as bond yield fluctuates.

Factoring better earning visibility and superior asset quality, at Rs 695, BoB’s share is trading 8.24 times its FY10 EPS.

HDFC Bank. HDFC Bank’s stock enjoys the highest premium among the large-cap banks. The reasons are obvious. It has consistently maintained a high growth rate without compromising on asset quality. Advances have grown by 39 per cent annually in the past three years. In spite of high growth, its asset quality is still one of the best in the industry, at net NPA around 0.3 per cent of net advances. The provisioning coverage is also high. Even though its provisioning policy is conservative (making larger provisions), the growth in profit is high and in the previous 42 quarters, it has maintained around 30 per cent annual growth in net profits. Because of high CASA deposit (around 50 per cent of the total deposits), the net interest margin of the bank is high and has helped it report high growth in net profit.

At a price-to-book value of four and PE of 29, the valuation may not rise, but growth in earnings would support the price rise.

Punjab National Bank. It is the most preferred choice among public sector banks. The differentiating factor is its ability to maintain high net interest margins. High CASA deposits in the overall deposit base helps it lower the cost of funds, while high lending to MSME (micro, small and medium enterprises) enable it price loans at higher rates. As a result, the NIM remains high.

Though there is a relatively higher risk related to restructured loan portfolios, the already high provisioning will ensure that the impact is minimal when the restructured loans turn bad. Another positive factor is that the value of the bank’s bond portfolio is less volatile as around 80 per cent of it is categorised as held-to-maturity, which is not marked-to-market.

At a price of Rs 1,017.05, PNB’s stock is trading 12 times FY10 EPS—a level attractive enough to ride on the bank’s growth.

Yes Bank. With the best asset quality and a strong growth rate, it is among analysts’ favourite stocks in the segment. At the end of the March 2010 quarter, the bank had a net NPA of just 0.06 per cent, while operating profits were up by 67.3 per cent compare to the same quarter last year. For the whole of FY10, the operating profit was up 63.6 per cent, while net interest income witnessed an upswing of 54.7 per cent. Interestingly, despite significant improvement in the CASA, Yes Bank's low cost deposits were at 10.5 per cent, much lower than large banks. Despite this, the bank had a net interest margin of 3.2 per cent, which is significantly better than most public sector banks.

Yes Bank has built its expertise in corporate banking and retail constitutes a very small part of its business. However, going forward, in the second phase of expansion (2010-15), it plans to accelerate its presence in commercial banking and aims to grow its balance sheet from the Rs 36,382 crore at present to Rs 1,50,000 crore. In terms of valuation, on a trailing 12-month basis, the stock is trading at 17 times.

Investors entering this stock are advised to take a long term earnings expansion play and not PE expansion.

Nice Article. Thank you for sharing the informative article with us. Stock Investor provides latest Indian stock market news and Live BSE/NSE Sensex & Nifty updates.Find the relevant updates regarding Buy & Sell....

ReplyDeletetax in india

equity shareholders