Though unable to beat their benchmark every year, some funds have done so convincingly over the long term.

If you have ever invested in a mutual fund (MF) scheme, or even watched an advertisement for one carefully, chances are that you would've come across the disclaimer: Past performance is no guarantee of future results. And you would do better not to dismiss it as a mere statutory requirement. Few investments mention the inherent volatility as candidly as this eight-letter sentence.

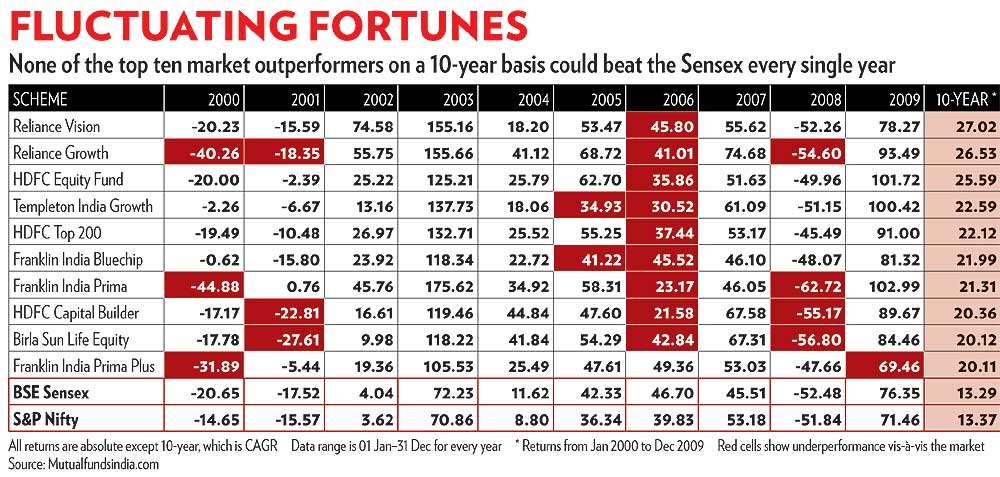

However, fallible as we are, most of us, consciously or unconsciously, resort to 'performance chasing'. As soon as we spot a hot fund or a fund that has sizeable exposure to a hot sector, we put our money on it, forgetting that lightning doesn't strike the same place twice. The result is that by the time we have made the investment the bull run is either already over, or in the deceleration mode. Plus, last year's champion might prove to be a dud this year, and vice-versa. In Fluctuating Fortunes, for example, take the year 2008. Few would have thought that previous years' champs would take such a nosedive. Almost every fund took a beating. Clearly, looking at the future is what matters.

Performance statistics

Every fund manager tries to outperform his respective benchmark index. However, if you look at the performance of all actively managed funds, few of them could outperform the widely tracked Sensex and Nifty on a 10-year basis. In fact, if you go by yearly returns, none of the funds could consistently outperform these two indices, not even the top 10 outperformers (see Fluctuating Fortunes).

When we looked at the performance of funds over 2000-2009, we found that the number of outperformers was more when the market did well. During the downturn, however, the number of underperformers exceeded that of outperformers. During the years 2000, 2001 and 2008, when the market gave negative returns, the number of underperformers was more. However, when the market returned a robust 76 per cent in 2009, more than 50 per cent of fund managers could not tap the opportunity, leading to underperformance.

Fund managers’ strategies

Usually, the fund manager of an actively managed fund exploits market opportunities by purchasing undervalued stocks or selling overvalued stocks. Either of these methods may be used alone or in combination. This way, fund managers check the market’s volatility and are able to deliver returns superior to that from the benchmark. Fund managers also use a variety of strategies to construct their portfolio, depending upon the fund’s mandate. Sometimes they purchase stocks that are temporarily out of favour with investors, or sell stocks at a discount to their intrinsic value, increasing the fund’s exposure to emerging sectors.

Why they fail

Fund mandate. This is a major limitation that fund managers face. In India, in order to be an equity fund, the equity exposure cannot be reduced to less than 65 per cent of the portfolio. This results in rising volatility and fund managers are not able to check volatility beyond a certain extent.

Poor investment decision. Poor investment decisions by fund managers could be the result of betting on sectors based on assumptions of their future growth, or buying into a stock at a wrong price at the wrong time. After all, it is not always possible to predict the unpredictable.

What you should do

Despite not being consistent performers on a yearly basis, there are several funds that have outperformed the benchmark indices by a wide margin over the long term. Investments in MFs are also supposed to be long-term. Therefore, we suggest that you don't jump at any fund just because it has done very well recently. Research thoroughly. And yes, keep reading Outlook Money. Every issue, we come up with OLM 50—our 50 choicest schemes across categories.

Despite not being consistent performers on a yearly basis, there are several funds that have outperformed the benchmark indices by a wide margin over the long term. Investments in MFs are also supposed to be long-term. Therefore, we suggest that you don't jump at any fund just because it has done very well recently. Research thoroughly. And yes, keep reading Outlook Money. Every issue, we come up with OLM 50—our 50 choicest schemes across categories.

No comments:

Post a Comment