If you are a retail investor, you should tread with caution in writing call options. Unlike buying a call option, where your loss is restricted to the premium amount, writing calls carry unlimited risk. Writing or selling a call option is a stand you take when you have a bearish view on the market. In options-speak, writing or selling calls are the same. Retail investors could opt for covered calls, that is write a call option only when one holds a reasonable amount of physical shares. Unlike buying a call option where you pay a premium, in writing call options, the writer of the option gets to earn the premium. Here’s an example of how it works.

The basics of call writing

Assume the Nifty is trading at 5,000 and you enter into a contract to sell a Nifty call option at 5,000 (strike price). This would imply that you are taking an obligation to sell Nifty at 5,000 on a future date (expiry date) irrespective of the price prevailing at the expiry date of the contract. Since you are bearing the risk on the call, you demand a premium of Rs 100 from the option buyer. The call option buyer pays you this premium. But the loss of the call option buyer is limited to the premium he pays, whereas your loss is unlimited.

How you lose big

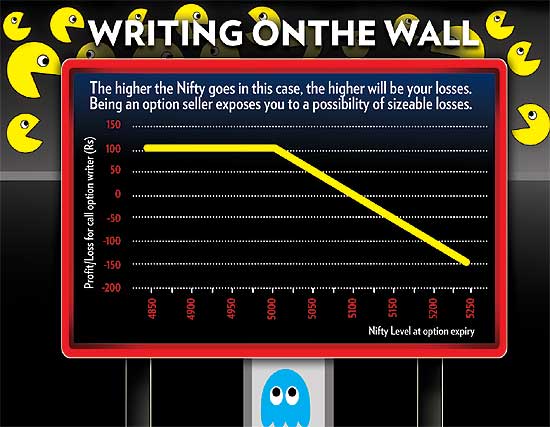

If on the date of contract expiry, Nifty is trading at a level below 5,000, say, 4,500, the buyer of the call option will ignore his right to buy at 5,000 since he is getting the Nifty at a cheaper rate from the market. But if Nifty is trading at a level above 5,000, say 5500, the buyer of the call option will exercise his right to buy Nifty from you at 5,000. So, as an option writer or seller, you will have to bear the losses. In this example, if the Nifty closes at 5,500, then the loss would be Rs 400, after factoring in the premium you received of Rs 100. (See Writing On The Wall). The higher the Nifty goes in this case, the higher will be your losses. The leverage factor magnifies the losses. Being an option seller exposes you to a possibility of sizeable losses, which could exceed the premium that you have charged the option buyer, which in this example is Rs 100. The chart shows that if Nifty settles at any level below 5,100 on the contract expiry date, you would not incur losses, which is after taking into consideration the premium you have earned.

Institutions love it

Options are more commonly written by institutional investors. One of the reasons is that institutional investors buy and sell stocks in relatively high quantities.

When they have determined a level at which they plan to off-load a sizeable quantity of a particular company’s stock, it would lead to a good amount of selling pressure as the quantity of sale of shares could be high. As a result, there is a fair chance that the share price would witness a resistance and find it difficult to overcome that level on the upside in the near term. To make the best of such opportunity, institutional investors would write a call option at that level.

Should you sell futures or write call options?

Both these stands are a bet on the market declining. When you go short on futures, you would benefit if the stock price declines. More the market declines, the more you earn. But when you have written a call you benefit even if the stock price stays where it is as you earn the premium. However your earning is restricted to the premium and does not rise in relation to the magnitude of fall in the stock price.

No comments:

Post a Comment