In January of 2009, when I wrote this column, I presented the readers of this magazine with the following table (Multiple effect). The table shows what happened in the past to the average returns over a three-year holding period for investors who invested in Indian equities (Nifty) at various levels of the market’s P/E (price/earnings) multiples. As one would expect the higher was the market’s P/E multiple at the time of investment, the lower were the subsequent returns.

As I write this, 2009 is about to end. Let’s see if the table’s conclusions were confirmed or contradicted by the market in 2009. When I wrote the January 2009 column, Nifty’s P/E multiple was 13.49 which is the cheapest range in the table. The table implied that if history is a good guide, then Indian markets should do well. In 2009 till date, Nifty has risen by 68 per cent, so one can say that history did prove to be a useful guide after all.

At present Nifty’s P/E multiple is 22.21, which, as the table shows implies that we should keep our expectations low. Are there other indicators which support my view and are there indicators which could prove this conclusion wrong? The answer is yes, and yes.

Let’s first look at supporting evidence. Let’s look at Nifty’s dividend yield over time. Let’s see what returns were earned by investors over one-year and three-year periods at various levels of dividend yields.

Multiple effect

The higher the P/E, the lower were the subsequent returns

| Nifty’s P/E (x) | Three-year returns (%) |

| Less than 14 | 152.10 |

| 14 - 16 | 112.39 |

| 16 - 18 | 79.14 |

| 18 - 20 | 51.18 |

| 20 - 22 | 21.18 |

| 22 - 24 | -14.98 |

| 24 - 26 | -32.92 |

| 26 - 28 | -36.60 |

| 28 - 30 | -40.17 |

The unique thing about this analysis is that I have not focused on average returns which can skew results. Rather, I have plotted all the data points on two scatter graphs.

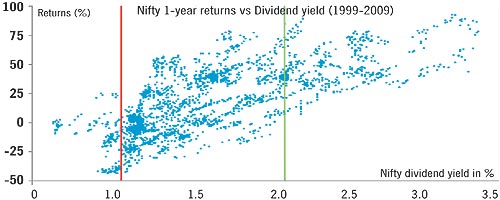

The graph below shows how investors fared over a one-year holding period when dividend yield was below 1 per cent, implying expensive market levels, between 1 per cent and 2 per cent, implying moderate market levels, and above 2 per cent, implying cheap market levels. All the data points since NSE started publishing data have been plotted on the chart.

As the graph shows, as dividend yield rose, so did one-year forward returns. High returns on equities were earned when Nifty’s dividend yield was more than 1.5 per cent.

|

So if history is a good guide, how likely is it that 2010 will be a very good year for equities? To answer this question, take a look at the left side of the scatter graph — the area covering all data points on the left side of the red line when dividend yield was less than 1 per cent. Notice that of all the days on which Nifty’s dividend yield was below 1 per cent, for most of such days the returns for the next one year were negative. There were some days when returns were positive but those were rare. Moreover, even on those rare occasions, returns never exceeded 30 per cent.

Will 2010 be one of those rare periods when satisfactory returns could be expected? I can’t say. What I can say is that history is telling us that we shouldn’t count on it.

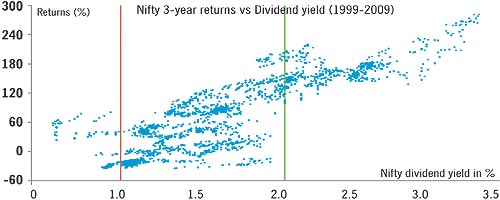

The graph, which covers three-year forward returns, tells the same story.

Yield that matters

On the days when Nifty’s dividend yield was below 1 per cent, for most such days the returns for the next one year and three years were negative. Nifty’s current dividend yield stands at 0.99 per cent

When Nifty’s dividend yield falls below 1 per cent, which is the case at present, Nifty has rarely done well over the next one year and three years.

Now, let’s look at some disconfirming evidence. Recent media reports claimed that the advance tax payments by Indian listed companies for financial year 2010 has risen by more than 30 per cent over the payments made last year. If this is correct, then it indicates that Indian companies expect higher earnings. Higher earnings imply higher dividends. If earnings are indeed about to rise, accompanied with a rise in dividends, then Nifty’s dividend yield at today’s market level would rise above 1 per cent.

The higher the yield rises, the more attractive will investing in Nifty become but low dividend yields are associated with low returns.

This does not have to mean that you should not invest in equities. After all there are several high quality stocks which have higher dividend yields and lower price/earnings ratios than Nifty.

My own view is that India is very well placed to create enormous wealth for long-term equity investors given its growth potential, and its high return on equity (among the highest in the world). While equity prices at present may have run a bit ahead of the underlying fundamentals, investors who keep their expectations low for the near term and continue to invest intelligently in Indian equities will have more than satisfactory results a decade from now and beyond.

Happy investing for 2010!

No comments:

Post a Comment