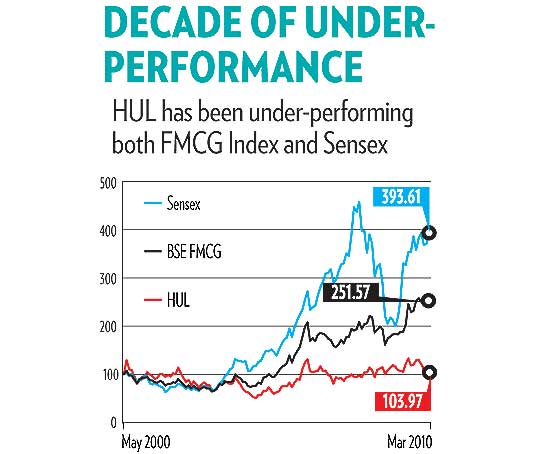

Hindustan Unilever (HUL), once the darling of investors, has remained unrewarded in the current market rally. It is the only stock that gave negative returns during this period. The quick answer to this is, even as other stocks moved up on prospects of better economic recovery, HUL has been bogged down by the recent spate of price wars in the FMCG industry. But what would you say of HUL’s share price over the last decade? It has remained at the same level even without price wars through the entire period. Does that mean the company has lost its sheen, or is it a case of market mispricing providing an opportunity to buy a good stock at cheap price?

Price war. In December 2009, P&G Home Products introduced Tide Natural, a new version of Tide, at a price lower than HUL’s Rin. HUL reacted by taking P&G to court, arguing the name “natural” is misleading. P&G followed this by cutting the price of its Tide soap bar. HUL retaliated by offering more detergent at the same price. The war reached its peak when HUL, for the first time, brought out an ad which made a direct comparison between its brand Rin and P&G’s Tide.This kind of price war is not new in the FMCG industry, but the severity seen this time was last witnessed in 2004. Then, P&G, cut the price of its two detergent brands, Ariel and Tide, to the extent of 50 per cent. Though HUL didn’t match the price cut, it did reduce the price of its brands Surf Excel and Surf Blue in the range of 30-40 per cent. Soon, the price war that was initiated in the detergent segment spilled over to other categories. The result was both companies took severe hits on their margins.

At first, the logic behind such a game looks simple. Says Aashish Upganlawar, an FMCG analyst at the brokerage firm Sharekhan: “Companies want to increase their market share.” Though market share comes at the cost of margin, companies take it differently. Adds Upganlawar: “Once you get the customer to your brand, you can concentrate on profitability later.”

The real game. Fighting for market share is a good strategy when the market for a product is limited, but it fails to explain why HUL and P&G are fighting, when there is scope for increasing per capita consumption of FMCG products as well penetration. The reason is found in the similarities in the price wars of 2004 and 2009. P&G started the war on both occasions, in the detergents segment. So it looks like P&G is aggressive in cutting prices. But why does it do so? A comparison between HUL and P&G’s product portfolio explains it. HUL has a product portfolio that has at least one brand for each section of the society (based on economic strata). For example, in detergents, Surf Excel is for the affluent, Rin is for the aspiring (middle segment) and Wheel for the striving. P&G till recently had failed to replicate this model in India. In detergents, it has Ariel for the affluent and Tide for the aspiring, but does not have a discount product for the striving class. This time around, during rising inflation, as HUL consumers downtraded, they moved from expensive to discounted products. For example, a consumer using Rin started buying Wheel. But even as this happened, they remained with a HUL brand. So, HUL’s volume grew but realisation did not improve. Meanwhile, P&G faced a real threat. If a consumer of Tide down-trades, there are no options left in P&G’s portfolio, and the consumer switches to some HUL brand or any other brand in the market. This time, P&G tried to bridge this gap by introducing Tide Natural at a price below its brand Tide. Say analysts Amnish Aggarwal and Nikhil Kumar of Motilal Oswal Securities in a note: “P&G has launched Tide Naturals at a lower price point to prevent loss of consumers to the economy segment.” It was also priced in the range between HUL’s Rin and Wheel to attract customers who down-trade from Rin or up-trade from Wheel. This alarmed HUL and the war began.

Why did HUL go wrong? Surprisingly, HUL has underperformed the overall sector growth in terms of top line and bottom line. If we look at the last ten years, HUL lies in the bottom quartile of the FMCG index. The CAGR net sales and net profit is 8.2 per cent and 9.87 per cent. P&G, on the other hand, has grown at 20 per cent CAGR in the last seven years. Sales and net profit growth of other players such as Nestle and Godrej Consumer Products are around 13 per cent and 20 per cent, respectively. Also, over the years, HUL has lost market share in most of the product categories it has a presence in.

Why did HUL go wrong? Surprisingly, HUL has underperformed the overall sector growth in terms of top line and bottom line. If we look at the last ten years, HUL lies in the bottom quartile of the FMCG index. The CAGR net sales and net profit is 8.2 per cent and 9.87 per cent. P&G, on the other hand, has grown at 20 per cent CAGR in the last seven years. Sales and net profit growth of other players such as Nestle and Godrej Consumer Products are around 13 per cent and 20 per cent, respectively. Also, over the years, HUL has lost market share in most of the product categories it has a presence in.

Some analysts consider this downward progression as natural. Says Anand Shah of Angel Broking: “HUL is in many categories, so it can’t outpace the industry. It is bound to lose market share in some of the categories. It’s just that in the last two years, the process has intensified.”

But there are larger issues at HUL that need to be mentioned. An important one is the change in management’s focus. Says Sanjay Singh of ICICI Securities: “There was a lot of focus on short-term earnings rather than long-term sustainability of the earnings. Earlier CEOs have been there for a very small period of time, so they tried to dress up the numbers while they were there.” Its profound impact is that HUL, which was earlier known for creating new market segments, seems short of innovations. Products like Lifebuoy and Close Up, which created altogether different markets, are now missing. Upganlawar seconded this view: “They haven’t been innovative enough to launch new products.” Figures from HUL’s parent company Unilever also support the fact that Unilever has not been competitive, compared to its peers like P&G, in spending on R&D that ultimately results in innovations.

What lies ahead? Though, for some time now, HUL does not seem be taking enough steps to stem the fall in its market share, the December-2009 (Q3FY10) result shows a change in HUL’s strategy. An example is the company’s efforts to maintain volume growth even if it had to match price cuts by its competitors. The positive impact is seen across almost all its brands, which gained market shares during the previous quarter. A sudden step-up in advertisement expenses to build brand value is another positive signal. It touched 14 per cent of the turnover in the previous quarter, compared to 9 per cent earlier. HUL has also re-launched many brands during this quarter to help the volume grow. The management tone has also changed. “Innovation” and “competitiveness” were used more often in Q3FY10 analyst presentations than in previous quarters. Though it is not talking about building a new market segment altogether, it does look focused on developing existing premium markets such as hair conditioners, surface cleaner and deodorants.

The most important transformation seems to be a change in the way the company rewards its executives. Says Singh: “Because you can’t keep the margin perpetually high and ultimately the growth has to come from volume growth, the focus on volume growth has increased. Earlier, the variable pay was more on bottom-line growth, but now it is a mix of market share (a direct consequence of volume growth) and bottom line.”

Your call. Although HUL’s management has indicated changes in its strategy, it is still to be seen whether it holds on to them in the coming quarters. Adds Singh: “In FMCG, even if you do something, the result may be visible six month or one year later.” So one thing is clear; the numbers from HUL might not look attractive in the next few quarters. However, you could take a call on company’s stock based on its valuation. Most of the time, its stock has traded at an earning multiple above 25, which has currently fallen to 22. Moreover, at the current price, its dividend yield is around 3, which is the highest among Sensex companies. When the price war ends, the share price could also appreciate. From the current level, the stock price does not seem to be going down much as market has already factored negative scenarios. So you can bet on HUL stock if you like steady stream of cash flows (dividends) and can wait for price appreciation.

Learning fundamental updates on stocks performance further help to decide whether investment should be made here or not. Service providers like epic research shares with fundamental reports as well.

ReplyDelete