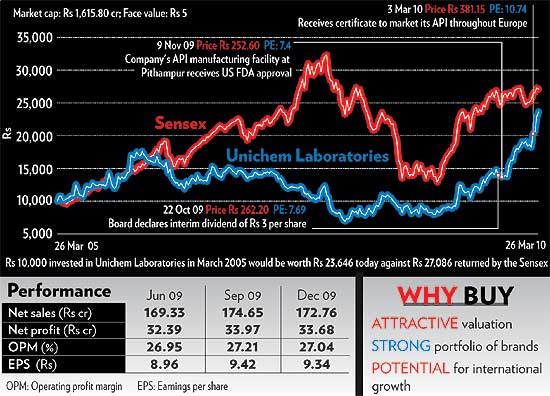

The risk of investing in a mid-cap stock currently is that you may end up buying it expensive even if the company’s growth prospects are high. Unichem Laboratories, a 66-year-old pharma company, is in a different group. Its growth is visible, yet its stock is available cheap (if you look at it separately or compare it with other companies in the BSE Healthcare Index). Unichem mainly manufactures formulations (the final product that is consumed by patients), and a small part of its revenue comes from active pharmaceutical ingredients (API; used in manufacturing final drugs).

Business performance. Unichem is mainly active in domestic formulations and the API market, which account for over 80 per cent of its total income. In the December 2009-end quarter (Q3FY10), its domestic income grew a healthy 18.51 per cent year-on-year (y-o-y). Both formulations and API businesses contributed—formulations grew 18.6 per cent and API grew 26.3 per cent.

In the domestic market, Unichem has a large portfolio of brands and is present in around one-tenth of the 1,495 therapeutic sub-groups tracked by the pharmaceutical market research company ORG-IMS. It is the leader in 17 therapeutic groups and among the top five in 69 therapeutic sub-groups. Its brands Vizylac and Ampoxin have a market share of as high as 33.2 per cent and 43.7 per cent, respectively.

One of company’s main strengths is its high-quality manufacturing infrastructure. While other Indian pharma companies are facing regulatory hurdles in penetrating the US market, Unichem is well set to grow fast there. Most of its manufacturing units are approved by the Food and Drug Administration (FDA), US, and it should not face regulatory hurdles in selling drugs manufactured at its India-based facility. The company has a strong pipeline of ANDAs (abbreviated new drug applications; required for selling generic drugs in the US) and has also got a few approvals. These indicate that the company’s international business is set to grow fast on the current low base.

Financial performance. Unichem has performed consistently over the years. Sales and net profit have grown at a compounded rate of 13.52 per cent and 28.60 per cent, respectively, in the last 10 years. Higher growth in profit than sales is a result of continuous improvement in its operational efficiency. The return on capital employed (RoCE) has risen from 15.77 per cent in March 2000 to 30.10 per cent at the end of previous quarter. The balance sheet is clean with a very low level of debt. Even then, the company has generated a high return on shareholders’ capital, with a return on equity of 22.40 per cent at the end of the previous quarter.

Investment rationale. Until recently, Unichem has been focussing on its domestic business, where it should continue to grow at a healthy pace given its strong brands, wide distribution and rapport with doctors. The next leg of growth will be from its international operations, which have a small base currently. Unichem already has regulatory approvals in the US for some of its brands. There are more in the pipeline. In the UK, it already has a presence through its 100-per cent subsidiary Niche Generics. The company assists in the sale and distribution of generic products in UK market, and it is expected to break even soon. This will boost Unichem’s bottom line in the future.

Given the visibility on Unichem’s growth, its stock is attractively priced even though its value has doubled in the last one year. At Rs 437, it is trading 12 times its annualised earnings per share for FY2010 as compared with the industry’s PE of 26.64.

No comments:

Post a Comment